Thomas Dickson, chartered financial planner at Wealthwide, reveals how dentists should respond to one of the lesser known but hugely significant consequences of Rachel Reeves’s autumn budget for their pensions.

Can it really be true that the latest budget means dentists’ beneficiaries might only receive 10% of pension funds on death?

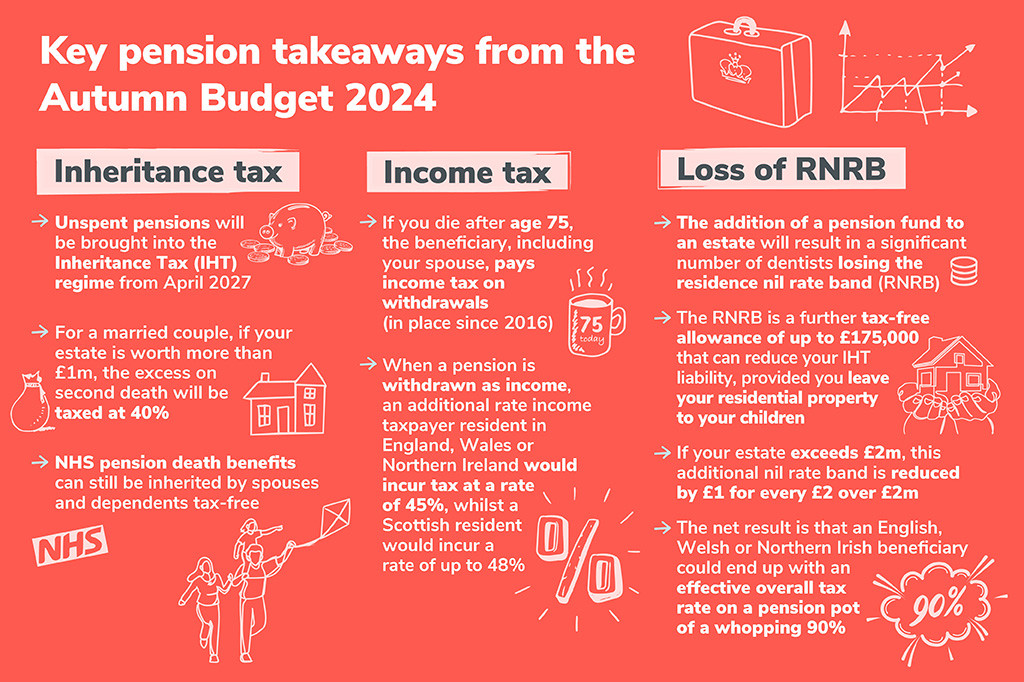

Chancellor Rachel Reeves announced that, from April 2027, unspent pensions will be brought into the Inheritance Tax (IHT) regime, meaning that if your estate is worth more than the nil rate band of £325,000, unless you leave your pension fund to your spouse or charity, the funds will be taxed at 40%.

But this change has other implications too – the actual tax take could be as high as 90%.

At Wealthwide, we have already started changing the advice we have been giving for decades. For example, we typically recommend clients leave the money in their personal pensions to spend last – ie to spend cash savings and ISAs first.

As a result of the budget announcement, we recently advised a couple encash their pension commencement lump sum now (up to the tax-free element of £268,275), and have that cash available to complete their house renovations and make further gifts to their children.

Of course, we were able to reassure them that they are financially secure despite the gifts so, provided they survive the seven years, they will be significantly reducing their inheritance tax liability.

Good news

There is some good news…

The NHS pension death benefits can still be inherited by spouses and dependents tax-free.

But unfortunately, it is back to the bad news.

The 40% inheritance tax charge is not the only tax charge. If you die after age 75, the beneficiary such as your spouse pays income tax on any withdrawals (although this has been in place since 6 April 2016).

Wait… it gets worse.

The residence nil rate band

For a significant number of dentists, the addition of a pension fund to an estate will result in them losing the residence nil rate band (RNRB). The RNRB is a further tax-free allowance of up to £175,000 that can reduce your Inheritance Tax (IHT) liability, provided you gift your residential property to your children.

If your estate, for IHT purposes (which, from April 2027, includes your pensions), exceeds £2 million, this additional nil rate band is reduced by £1 for every £2 over £2m, meaning someone with an estate of £2.35m will have no residence nil rate band (RNRB) available to them.

It is therefore possible that a dentist with assets of £2 million and a pension pot of £350,000 could find a 40% IHT rate applies to the pension and overall estate due to the loss of the RNRB of up to 60%.

When the pension is then withdrawn as income, a further layer of tax is applied to the pension funds. An additional rate income taxpayer resident in England, Wales or Northern Ireland would incur tax at a rate of 45% on such funds, whilst a Scottish resident would incur a rate of up to 48%.

The net result is that an English, Welsh or Northern Irish beneficiary may only receive as little as £36,787 additional cash from the £350,000 pension pot. That works out as an effective overall tax rate on the pension pot of 89.49%. A Scottish beneficiary of the estate would receive even less in these circumstances.

This is undoubtedly going to have substantial implications for estate planning and intergenerational wealth transfer.

Long-term security

I mentioned the above issues to a retired dentist this week and he told me he had met some dentists at an event recently who explained they each had £1 million in their pensions. He asked them what the money was for and they said: ‘It’s for the kids.’

As a long-standing Wealthwide client who has heard us talk about ‘living the life you want’, he encouraged his colleagues to use the 25% tax-free cash of £250,000 each and do all the things on their ‘bucket list’.

I really hope these dentists have taken his advice as the alternative is that, if they don’t spend it, HMRC is likely to get a significant share on their death.

Please remember your long-term financial security should always be the foundation of any decisions you make. While tax is a crucial component of sound financial planning, it should not be the sole driver of any strategy.

It is also important to note that these changes will not take effect until April 2027 and transfers between spouses on death will remain outside of the IHT calculations even after that date.

If you would like to know how these changes might affect your personal circumstances and if you are keen to leave a legacy to your beneficiaries rather than to HMRC, please do get in touch.

Investment risk

Please be aware of the following investment risks

- The value of your investment can go down as well as up and you may not get back the full amount invested

- When investing your capital is at risk

- Levels and bases of, and reliefs from taxation are subject to individual circumstances and may be subject to change

- The Financial Conduct Authority does not regulate taxation and trust advice.

To better understand the impact of the Budget on your retirement plans with the support of a financial expert, do get in touch and we can help you make sure you’re still on the right track.

Wherever you are on your financial journey, if you want some visibility over your finances, take our quick quiz, the Financial Freedom Scorecard – it only takes two minutes to complete!

This article is sponsored by Wealthwide.